[Excerpt from the January Austrian Investing Monthly Newsletter. Download free at St Onge Research.]

[Excerpt from the January Austrian Investing Monthly Newsletter. Download free at St Onge Research.]

Does cheap oil cause recession?

Not when Oil Supply is Soaring.

For the past year, the price of oil has been plunging, spooking markets going into year-end. Oil is one of Wall Street’s favorite recession indicators. So are they right to worry?

In short, no. Falling oil prices today are supply-driven. Meaning that today’s cheap oil is a boom indicator, not a recession indicator. Because cheap credit subsidizes investment, and oil is one of the most capital-intensive industries out there.

It’s actually better than that: falling oil prices are great for the rest of the economy. Suggesting that cheap oil itself contributes to keeping the boom going.

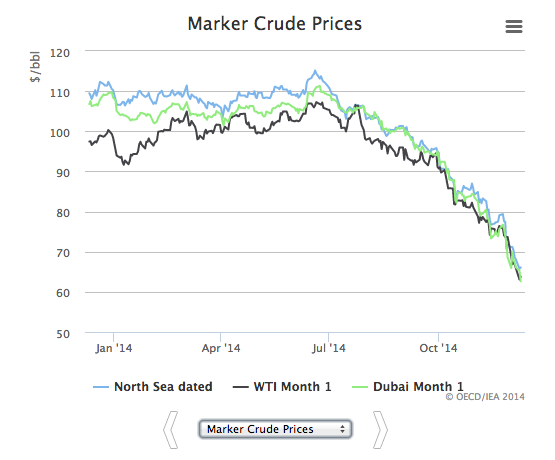

First, the data: from the International Energy Agency, oil prices have fallen by more than half since June, 2014, from $107 on benchmark WTI to under $49 today.

When you see a price move the first thing to ask is whether it’s coming from supply or demand. Is oil falling because there’s more oil, or is it falling because people aren’t buying as much?

The answer, so far, is supply: the IEA estimates that global oil demand rose by 1.4 million barrels per day, while supply rose by 1.7 million barrels between Q1 2014 and Q3 2014. The rise isn’t just Dakota frackers; OPEC’s output rose in-line with overall supply.

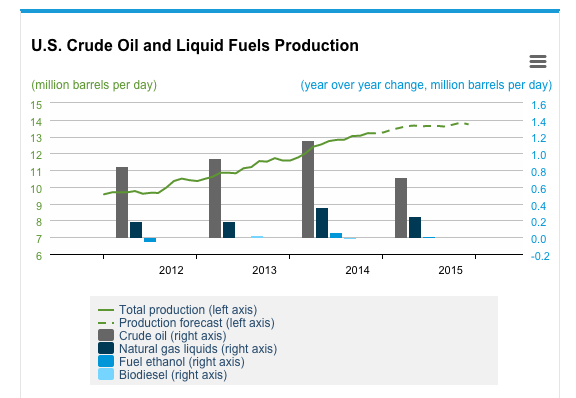

Zeroing in on the US, the story is even more dramatic: healthy demand vs even healthier supply. Check out the charts below: demand is “liquid products supplied” and supply is production. The other usual suspects, China and Europe, are both using oil normally as well (see charts next page).

The bottom line is healthy but not soaring worldwide demand, consistent with the later boom stage of the cycle. Paired with soaring supply, this gives us lower prices.

So if demand is stable, why is Wall Street so worried about cheap oil?

So if demand is stable, why is Wall Street so worried about cheap oil?

Two reasons. First, statistically, oil prices correlate with recessions. And, second, they worry that cheap oil might hurt the economy in other ways.

Let’s unpack these concerns. First, the correlations. Wall Street analysts run on statistics, not theory. Statistics are a beautiful thing, but one of their biggest strengths is also a big weakness. In particular, statistics cancel out noise. Meaning that one-off events disappear from statistical analysis. So if you’ve got frequent replicable events — say, rainy days and umbrellas — then statistics are your friend. On the other hand, if you’ve got rare events — say, fracking booms — then statistics will give you the runaround.

This means Wall Street is running with the correlations, which come from the most common event affecting oil prices — drops in demand. Drops in demand for oil absolutely correlate with recessions, since a drop in demand suggest businesses are using less oil.

This means Wall Street is running with the correlations, which come from the most common event affecting oil prices — drops in demand. Drops in demand for oil absolutely correlate with recessions, since a drop in demand suggest businesses are using less oil.

On the other hand, supply disturbances, while common in oil, are each unique. Libyan rebels, the Suez closing, subsidies paid for exploration, fracking. Each is unique. And correlations are actually intended to eliminate unique events as “noise.”

So what’s happening today is a rare (in a statistical sense) event, which is a secular rise in oil supply.

Now, “rare” doesn’t mean “noise” that we can just ignore. Indeed, this rise in supply is a very useful cycle indicator, just not in the way Wall Street thinks. It’s an indicator of cheap money. Oil exploration and development takes scads of money, and cheap money subsidizes that investment. Meaning that cheap money increases the supply of oil.

This means that a falling price due to rising supply is actually a boom indicator. Specifically, it’s a late-boom indicator, telling us that money’s been cheap long enough to subsidize lots of new oil projects to fruition.

This means that a falling price due to rising supply is actually a boom indicator. Specifically, it’s a late-boom indicator, telling us that money’s been cheap long enough to subsidize lots of new oil projects to fruition.

Now, this isn’t exactly news. We already know that the boom’s late-stage simply because we can see how low rates have been. The Fed’s been feeding this boom for a good 6 years now. Oil prices are giving us no new information — they’re simply a confirmation. They’re simply what happens when you feed the world cheap money for 6 years — you get oversupply of capital-intensive goods.

Now let’s consider the second question, whether oil prices will hurt the rest of the economy. It’s actually a bizarre question to even ask; I guess analysts who don’t  know theory just read off the correlations and wave their hands at what happens in-between. Why bizarre? Because cheap stuff makes the economy grow. Cheap stuff means there’s more to spend on other stuff. So cheap oil means more money going to iPads, movies, vacations, whatever. It’s an unmitigated good for the rest of the economy.

know theory just read off the correlations and wave their hands at what happens in-between. Why bizarre? Because cheap stuff makes the economy grow. Cheap stuff means there’s more to spend on other stuff. So cheap oil means more money going to iPads, movies, vacations, whatever. It’s an unmitigated good for the rest of the economy.

So if the price of oil today isn’t important as recession indicator, what should you watch instead? Demand. In particular domestic demand for oil. If this starts falling, then you’ve got a genuine recession indicator. And that’s when to fret.

What about the future price of oil? Oil is a very a noisy indicator – remember those frequent “unique” events. So the best we can say is what the cycle will do. And the cycle trend is weak (i.e. it won’t overcome noise) for the short-term, until either Europe and China get worse, or until the US economy starts to turn down. At which point oil starts really getting its demand-driven price drop to go along with that supply-driven drop.

At that point, when the recession is coming, will prices go down? Again, cycles only give trend with a price as volatile as oil. So the price will tend to fall, but who knows if it will. For example, if a US downturn shutters fracking massively, or makes it hard to finance new oil exploration, then price could actually rise in a recession. So we want to be careful to know what’s driving prices, on both supply-side, demand-side, and any outside noise.

(This, by the way, is why commodities investment is not for beginners. You really do have to live and breathe a commodity to invest competently. There’s always something you missed — oh, I forgot Qaddafi might get shot and Libyan refineries closed for a year.)

Finally, whither fracking? The old-hand investors in natural resources know this, but resources is no place for widows and orphans to invest. Fracking today is levitating on a flood of easy money. And, when that money cuts off, many fracking investments will be under-water. Expect a bust when the smoke clears, intensifying after interest rates start rising. For now, if you’re running a $5,000-a-spot trailer park in North Dakota, enjoy the boom but do put something aside for the bust.